You practically have to be in the Forbes 500 to own a club like Man United in the modern era – so could another one of the world’s wealthiest people soon join Sir Jim Ratcliffe and the Glazers in M16?

Enterprise values of Premier League clubs have risen dizzyingly fast in recent years thanks to a mixture of soaring media income and interest from the private equity and sovereign wealth sectors.

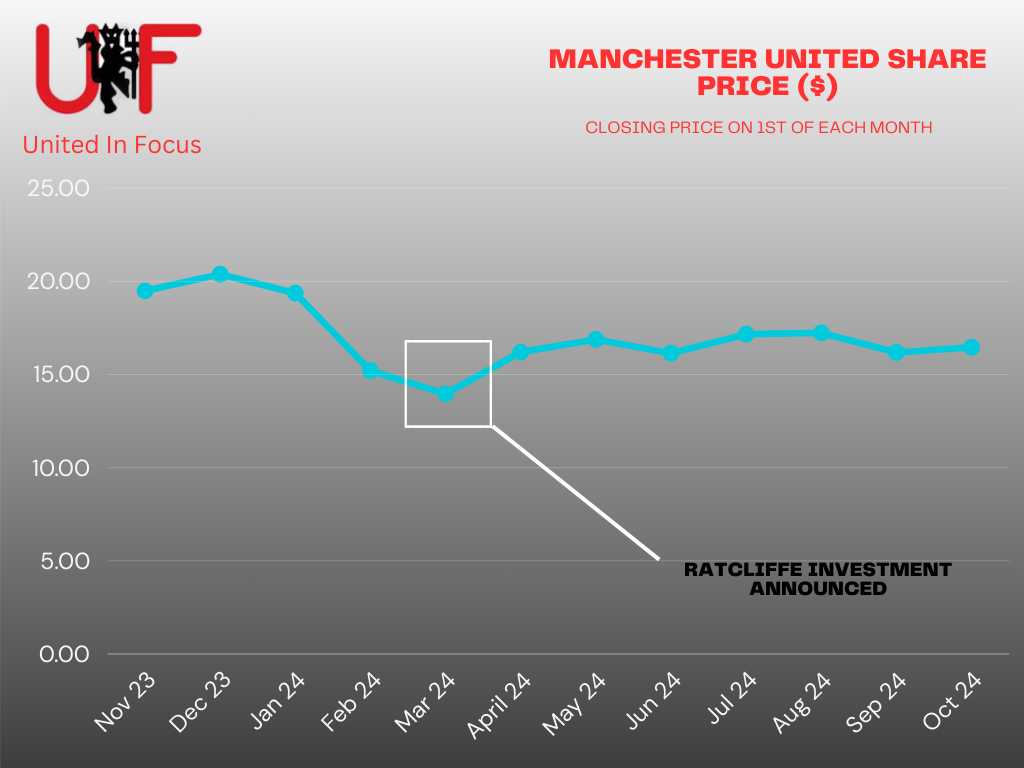

Ultimately it’s subjective, but most experts suggest Man United are worth around £4bn in total. That appraisal scans given that Sir Jim Ratcliffe paid £1.25bn for a 27.7 per cent stake in the club in February.

However, the Glazers – who still own just under half of the club’s shares and the majority of its voting rights – think that £4bn actually undervalues the club.

That is why the six siblings and their advisors pivoted away from a full takeover last year, rejecting an outright bid from Sheikh Jassim that valued United at £5bn.

Meanwhile, Man United’s market cap (the aggregate value of the 22.5 per cent of the club’s shares traded on the New York Stock Exchange) is around £2.4bn at the time of writing.

Market cap is an imprecise way of measuring company value, but that figure does suggest that the big brains in the world of finance think Ratcliffe and Ineos’ investment undervalued the club.

Former United CEO Ed Woodward once snarked that United don’t need silverware to be commercially successful and, nauseating as his sentiments were to fans, they were more or less on the money.

Granted, recent years have seen growth in the two revenue metrics that are fundamentally within United’s control, commercial and matchday income, slow down.

But new manager Ruben Amorim is walking into a club starved of a Premier League triumph for over a decade but which still generated more income than all but four clubs in world football last season.

It is a resilience that won’t last forever and does not excuse the complacency-turned-neglect that the Glazers have exhibited in the last decade. It does, however, indicate just how strong United’s brand is.

That term, ‘brand’, is one that bedrock supporters can’t stand – and justifiably so. United were founded as a club, not a vehicle to sell merchandise and advertising space.

But it is United’s IP that investors are interested in. That’s their badge, player image rights, the license to trade off United’s history and heritage. Basically, anything that helps sell products, services or experiences.

United are set to either move into a new stadium or make sweeping changes to Old Trafford. Either way, it will be monumentally expensive.

And that means the value of the club as a brand and a business has never been more important.

Man United to take on fresh investment to fund new stadium?

Man United need a new home or a major refurb.

But with costs in either scenario likely to run north of £2bn, funding is a very real issue.

The Glazer family and Sir Jim Ratcliffe are asset rich and independently wealthy, of course, but they are unlikely – especially in the former’s case – to front much of their own cash for the stadium project.

For one, they might not have the liquid capital. And even if they did, it makes more sense for them to use external funds.

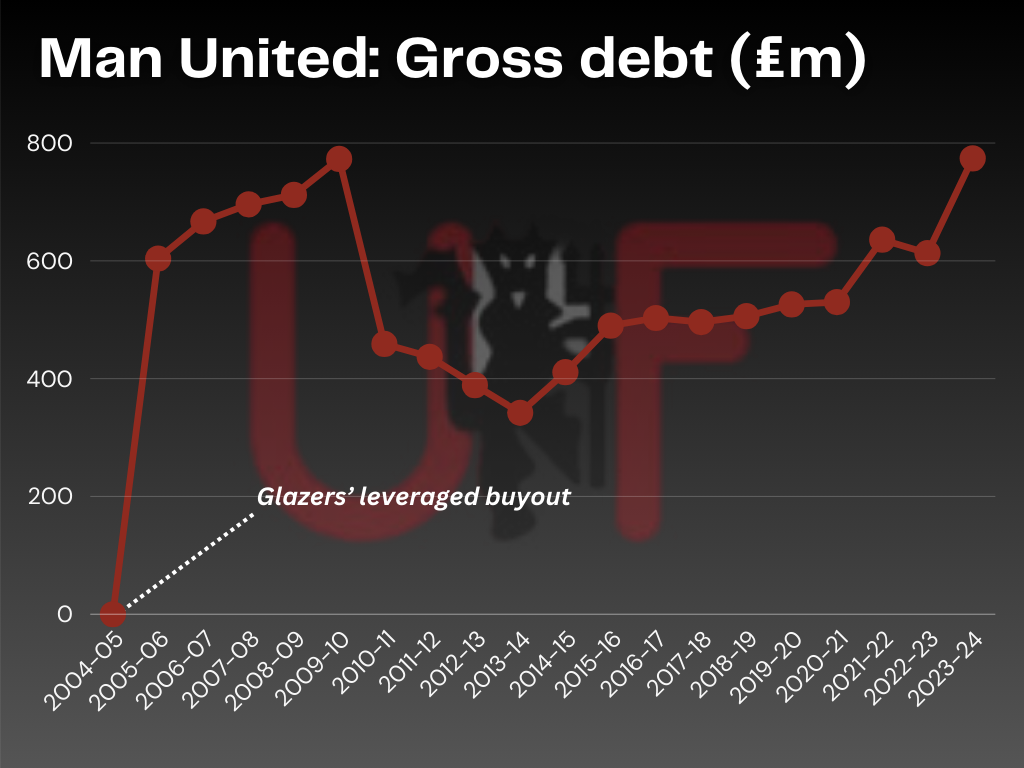

Most capital expenditure projects of this magnitude rely on a combination of loans, bonds, and credit facilities.

But United already have huge gross debt and, as former Man City adviser and football finance expert Stefan Borson points out, would struggle to raise and service another £2bn in commercial loans.

Writing on X, Borson said: ‘[A] substantial amount of equity is the only realistic option. So that’s either Ratcliffe, Glazer or a new equity partner.’

Quoting a post detailing the interest rates Chelsea, who also want to rebuild or move homes, are paying on their loans with Ares, the regular talkSPORT analyst said more Ratcliffe equity investment is most likely.

However, a new equity partner – i.e., a group or individual who would provide billions in capital in exchange for a stake in the club – is also a possibility.

Ineos and the Glazers’ options: Private equity

The pool of investors who can afford to stump up hundreds of millions or billions is very shallow.

The pool of investors who think it makes good business sense to spend that kind of money on a football club is even more so.

United have lost £341m over the last five financial years and have averaged a deficit of around £17m since Malcolm Glazer’s takeover in 2005.

There was, however, plenty of interest when the family put the club up for sale at the back end of 2022.

Most of that came from private equity titans like Carlyle and Apollo, who are among the richest companies on the planet.

Typically, private equity firms want a return on their initial outlay in five to seven years in order to satisfy their limited partners, the high net worth individuals who trust them with their money.

There is recognition within the private equity sector that that sort of timeframe is not realistic within football, where they are banking on technology to monetise global fanbases in coming decades.

But given that these firms are typically more satisfied with being a silent or less active partner within an ownership structure, private equity could be a smart choice for the Glazer-Ratcliffe alliance.

Could a Middle East sovereign wealth fund buy a stake in Man United?

For many supporters, regardless of the attached concerns about human rights and sportswashing, an oil-rich sovereign wealth fund is the dream owner.

Newcastle United, Paris Saint-Germain and Manchester City have this model, with Gulf states having bought the clubs with the apparent aim of getting a cultural foothold and improved image in the West.

When Sheikh Jassim, a mysterious Qatari banker and member of the nation’s royal family, tried to buy United his aim was to acquire 100 per cent of the club.

It is unlikely that any sovereign wealth power would be content with a minority stake in the club unless it was one that came with significant operational input, like Ratcliffe’s has.

In any case, the royal families of Gulf states often include thousands of members. There are 15,000 royals in Saudi Arabia, for example. Not many of those can afford to buy a Premier League club.

Sovereign wealth is not the monolith it is often made out to be, although the nature of Gulf nations’ economies is that the state almost always has some oversight.

In any case, there are a limited number of funds like PIF or QSI and UEFA’s conflict-of-interest rules means that most already have their one outpost in European club football.

It seems an unlikely option for United in this context.

Receive a digest of our best United content each week direct to your mailbox