Debt isn’t a dirty word in finance – the opposite, in fact. Good debt fuels growth and, in theory, makes everyone a winner. But at Manchester United, the banks and the Glazers are the only ones winning.

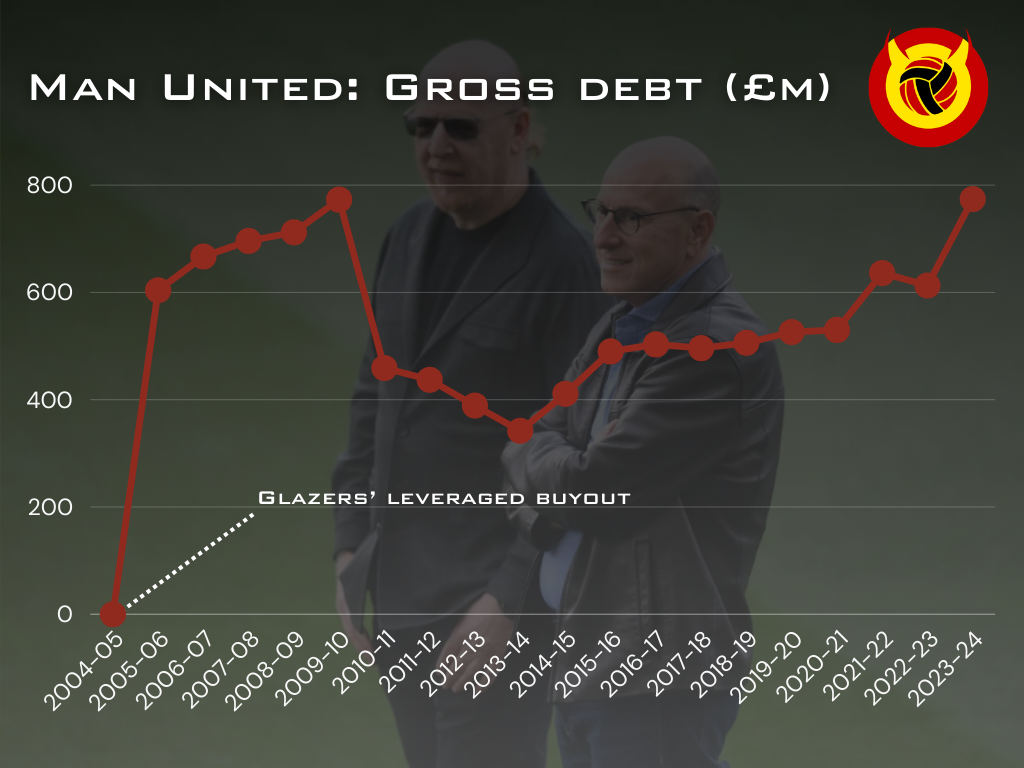

The family’s leveraged buyout of United in 2005 loaded the club with £604m worth of debt. It was hoped that 2012’s New York Stock Exchange listing would ease the burden, but it barely made a dent.

As it happens, the Glazers pocketed around half of the proceeds from initial public offering in the United States. And in March 2025, United’s gross debt is £731.5m. That’s £127m more than 2005.

Okay, the real-terms value of the debt has fallen when adjusted for inflation. But the Red Devils have paid over £750m in interest since the takeover, wiping out the difference and then some.

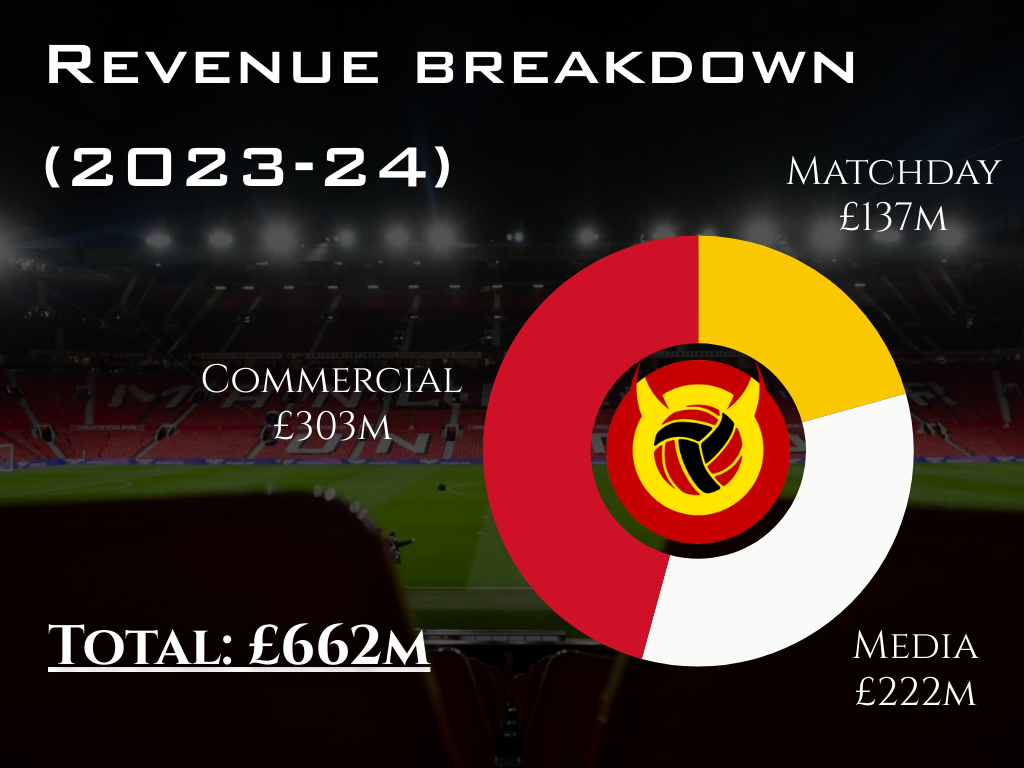

But so what? United are only paying around £30m per year in interest, compared to club-record revenues of £662m in 2023-24. Chump change, right?

For a club in better financial nick, maybe. Tottenham, for example, earn less than United and pay a similar amount in annual interest. But unlike Spurs, United don’t have a money-printing stadium to show for it.

What’s more, Spurs aren’t haemorrhaging cash. In terms of cost control, the two clubs have been poles apart in recent seasons, in contrast to their proximity to one another in the Premier League table.

| Position | Team | Played MP | Won W | Drawn D | Lost L | For GF | Against GA | Diff GD | Points Pts |

| 13 | 27 | 10 | 3 | 14 | 53 | 39 | 14 | 33 | |

| 14 | 27 | 9 | 6 | 12 | 33 | 39 | -6 | 33 |

Sir Jim Ratcliffe is attempting to curb that, although his methods – mass staff cuts, removal of basic perks, and reducing charity and community spending – have crossed a line between efficiency and ruthlessness.

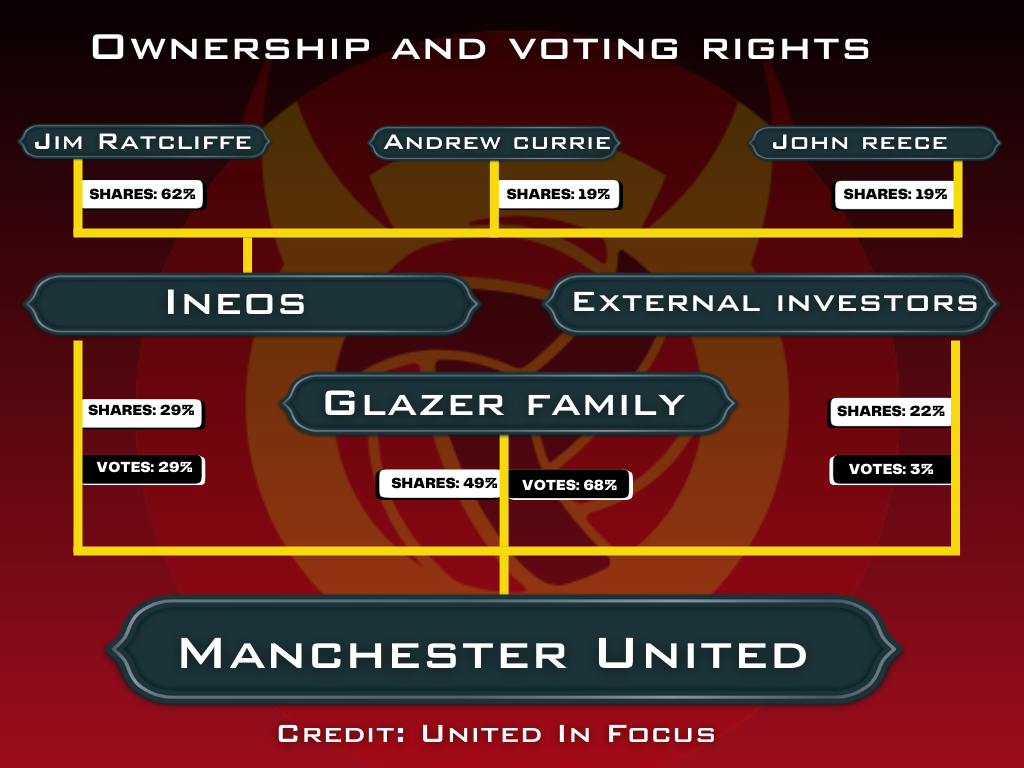

Ineos, who own 29 per cent of United’s equity but have been handed operational control by the Glazers, have been equally brutal in their campaign to boost revenue to service the debt.

Ineos have increased ticket prices at Old Trafford and, in line with a worrying trend across the English top flight, are scaling concessionary pricing for juniors and seniors.

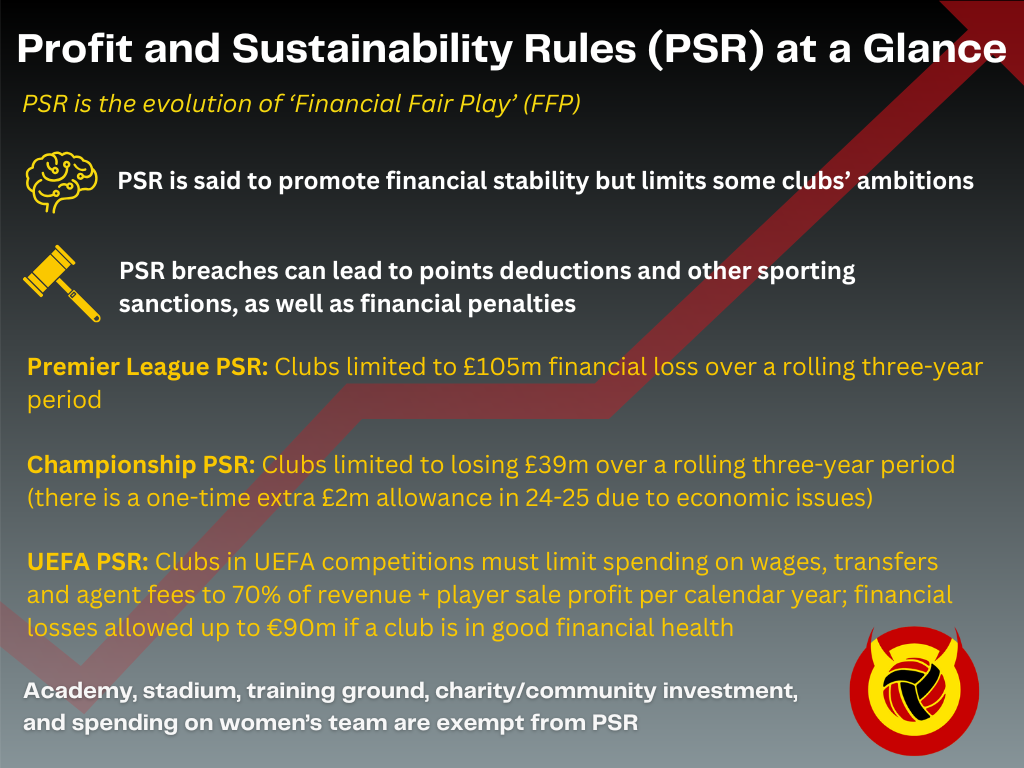

Meanwhile, the Premier League’s decision to retain Profit and Sustainability Rules (PSR) for at least one more season means United’s interest payments will continue to eat into Ruben Amorim’s budget.

Incidentally, UIF understands that Crystal Palace, not United, were the only team to vote against the retention of PSR and the delay of a UEFA-style squad cost rule.

Although, that may simply have been herding in the face of the inevitable at the recent Premier League shareholder meeting in London where the vote was held.

Either way, Ineos have their work cut out juggling United’s financial situation with the mess they have inherited in the football department.

But, as Liverpool University football finance lecturer and industry insider Kieran Maguire has explained in exclusive conversation with UIF, things could get worse before they get better.

Man United’s debt costs set to soar ahead of 2027 cut-off, says Kieran Maguire

Of United’s £731.5m debt, the breakdown is as follows:

- Senior secured notes: £337.6m

- Secured term loan facility: £178.1m

- Revolving credit facilities: £210m

- Accrued interest: £5.7m

The senior secured notes (mostly bank loans) and the revolving credit facility (the club’s overdraft), reach maturity in 2027.

In layman’s terms, United either have to pay off the principal – £548m in total – in its entirety or refinance, AKA negotiate new terms with the lenders to spread the cost out over a new term length.

“With some of Man United’s current loans maturing in 2027, there is a concern,” warned Maguire.

“Global interest rates have increased since the loans were originally taken out, so there could be an additional interest burden.

The Manchester United Supporters Trust, or MUST, recently published analysis that forecasts that United’s interest payments could double after 2027.

“On a separate issue,” says Maguire, “the new stadium is in the process of being engineered and approved, then the club will have to borrow further from the market at a time of high interest.

“Long-term interest rates are around about four and a half per cent and there could be a premium on top of that in terms of interbank.”

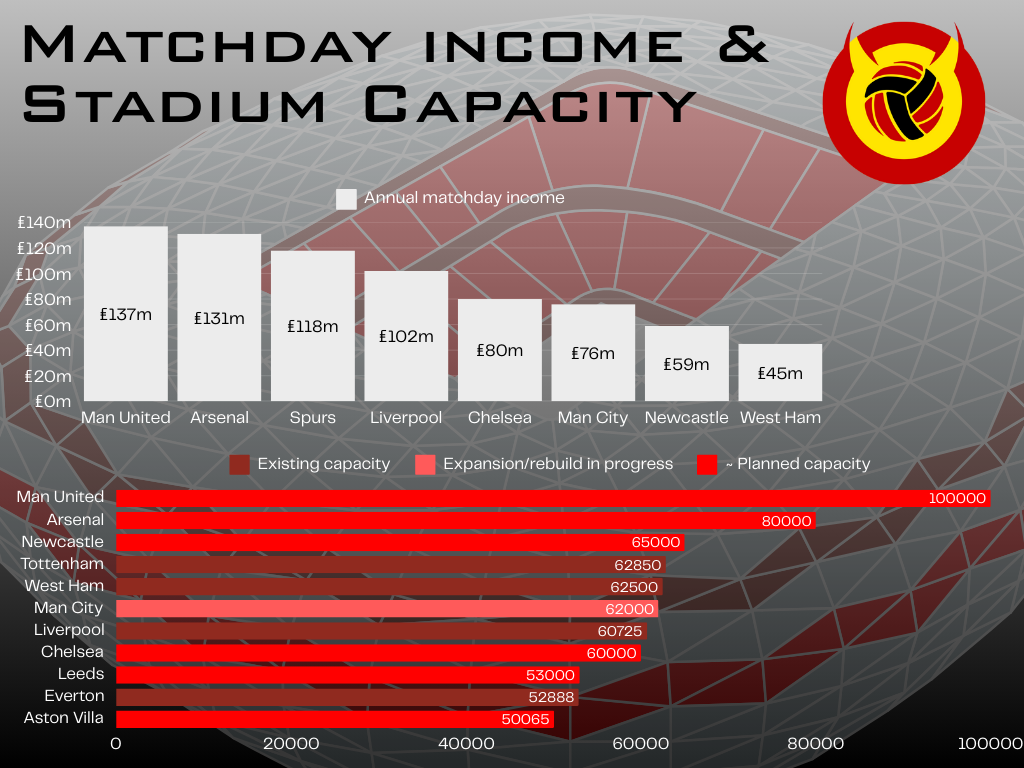

Old Trafford expansion or rebuild: United’s debt salvation?

“It’s not a good time to borrow – and that is far from ideal for Man United,” explains Maguire.

“Certainly, United’s interest costs could rise substantially and quickly. There’s no doubt that the debt is the biggest problem facing the club, in my view.

“However, if they get additional revenue coming from the new stadium, you have to look at it on a net basis.”

United are leaning towards a new 100,000-seater stadium, whose cost will run well into the billions.

“If you’re generating more money from the new Old Trafford project, you have to look at how much is coming in to see whether or not they will better off financially.”

Based on a crude pro-rata calculation taking into account United’s current matchday income and capacity, a 100,000-seater stadium would generate £183m through the turnstiles annually.

In reality, however, the final figure would be much, much higher due to plans to focus on the lucrative corporate hospitality sector, in-stadium revenue maximisation, and associate commercial benefits.

Most experts UIF have spoken to think £250m is a realistic estimate.

Ed Woodward wrong about United’s debt but set for job with Premier League billionaire

In the final analysis of United’s demise over the last decade, there are myriad individuals one can pin the blame on.

Alongside the Glazers themselves, a string of myopic managers, big-name flops, and a racehorse named the Rock of Gibraltar, most United fans will point to Ed Woodward as the arch-villain.

The blazered, former investment banker was – by his own admission – more into rugby than football.

He was also more into short-term commercial dopamine fixes than the long-term financial health of the club.

United’s debt position becoming increasingly insidious during his time at the club, which formally started in 2007, two years after he helped broker the Glazers’ leveraged buyout.

Famously, he said United don’t need to win trophies to make money. And when he said that in 2013, it looked like he was spot on. In 2025, however, his short-sightedness is being exposed.

Yes, United remain one of the richest clubs in the world by turnover. But they have stagnated commercially and other, smarter teams are set to surpass them soon.

On debt too, Woodward’s parochialism is being shown up. “The interest on the debt is £20m or something,” he said in the summer of 2014. “That is less than 5% of our revenue.”

But, coupled with abysmal cost control and zero progress on the pitch, the debt is now a significant drain on resources that could – and should – otherwise be going towards the restoration project on the pitch.

But the former JPMorgan man’s CV has not put off John Textor, the largest individual shareholder at Crystal Palace.

Textor has offered Woodward a new job, as a director of his multi-club empire, Eagle Football.

In a move that has, it is fair to say, confounded the football finance industry, Eagle Football are preparing to float on the New York Stock Exchange.

Woodward, who was made executive vice chairman two years after the Glazers listed United in New York to reduce the club’s debt, has experience running a public company.

But supporters of the clubs owned by Eagle – Palace, Botafogo, Molenbeek and Lyon – will surely be wary given the 53-year-old’s controversial tenure at Old Trafford.

Receive a digest of our best United content each week direct to your mailbox