Manchester United under the corporate management of Sir Jim Ratcliffe and Ineos’ various enforcers at Old Trafford have borrowed liberally from the Donald Trump playbook of late.

Trump’s administration have a tactic they call ‘flooding the zone’ when they want to bury a story with a media blitz – and in 2025, there has been something of that in Man United’s communications too.

For the regime at the White House just as it is at Old Trafford, it’s about hitting the press with so many stories, angles and morsels that their attention and resources are simply spread too thin.

As a result, none of the issues get the attention and dissection they deserve. Think Ratcliffe’s bombshell round of interviews in March, followed by the confirmation of plans to build a new stadium 24 hours later.

In communications, the received wisdom was historically that less is more. Now, that convention is being subverted by Trump, Ineos, and indeed many bad faith actors in football finance.

Ratcliffe’s chemicals firm has explicitly thrown its weight behind Trump 2.0 in the past. Incidentally, so has Edward Glazer, who donated a seven-figure sum to his campaign.

Ineos chairman Brian Gilvary has praised the administration’s policies on oil and gas, which he says are in stark contrast to Labour’s “negative” approach to business and, specifically, offshore drilling licenses.

And yes, this is relevant to United in a real, material way. Ineos are experiencing cash flow issues at present, which could restrict their ability to externally fund Ruben Amorim’s summer transfer budget.

Moody’s, the credit ratings agency, recently changed Ineos’ credit rating to ‘negative’, which could be a problem when the Red Devils are looking to secure cheap debt to fund a 100,000-seater stadium.

| Stadium | Cost (adjusted for inflation) | Location | Opened |

| SoFi Stadium | £4.25bn | California, USA | 2020 |

| New Man United Stadium | £2bn (est) | Manchester, UK | 2030 (est) |

| MetLife Stadium | £1.5bn | New Jersey, USA | 2010 |

| Allegiant Stadium | £1.5bn | Nevada, USA | 2020 |

| Wembley Stadium | £1.45bn | London, UK | 2007 |

| Yankee Stadium | £1.4bn | New York, USA | 2009 |

| AT&T Stadium | £1.4bn | Texas, USA | 2009 |

| Mercedes-Benz Stadium | £1.2bn | Atlanta, USA | 2017 |

| Singapore National Stadium | £1.1bn | Kallang, Singapore | 2014 |

| Tottenham Hotspur Stadium | £1bn | London, England | 2019 |

| Optus Stadium | £900m | Perth, Australia | 2017 |

United could receive some relatively modest grants for infrastructure around the stadium from the UK government meanwhile, though Rachel Reeves may not take too kindly to Ineos’ stance on her policies.

Similarly, Ratcliffe’s stance on more red tape in football via a government-backed independent regulator, which he opposes, might also not curry much favour on Downing Street.

And, back at United HQ, Reeves’ initiative to raise employers’ national insurance contributions by 1.2 per cent – which took effect on 6 April – will increase United’s wage bill by several million pounds annually.

In short, Manchester United’s finances are at the mercy of political and economic headwinds.

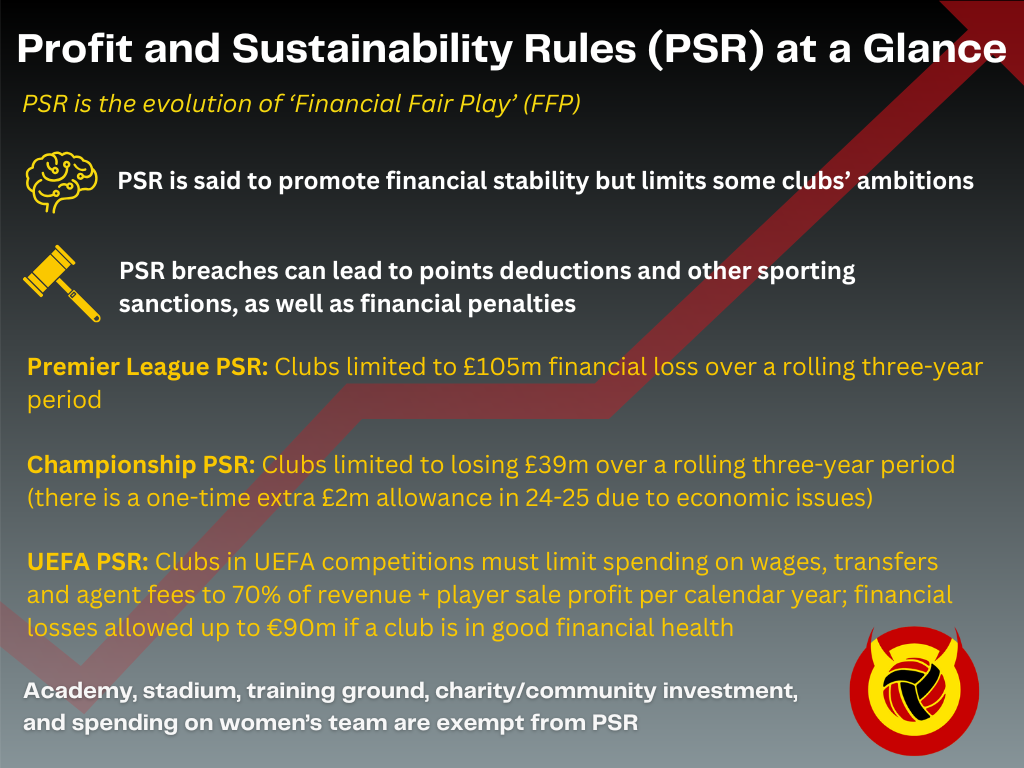

And, with the margins very tight at the club as it stands, the Ratcliffe regime’s ability to operate within Profit and Sustainability Rules (PSR) and fund a gravely needed revamp of the squad has been shaken.

Re-enter, Donald Trump, an unlikely figure in United’s PSR saga.

American economic volatility could eat into Man United’s PSR quota

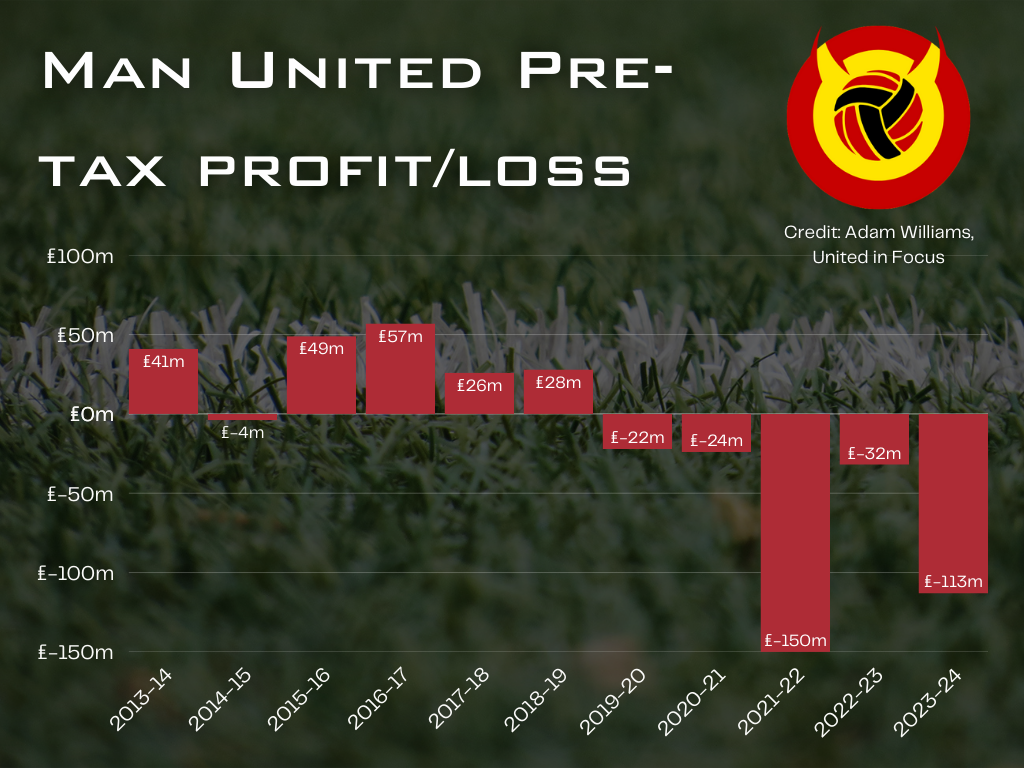

Under the Premier League system (UEFA have their own, distinct set of rules), PSR limits Man United to losing a maximum of £105m over a rolling three-year period.

You will probably be aware that, despite remaining one of the richest football teams on the planet by revenue, the club has lost far more than £105m over the last three completed seasons.

United have not yet fallen foul of Premier League PSR as the rulebook makes allowances for infrastructure investment, lost revenue as a legacy of the pandemic, and expenses related to the Ineos takeover.

However, as Ratcliffe made clear in his open letter to several supporter groups in January, it’s a close-run thing. This is the reason, he says, mass redundancies and increasing ticket prices have been necessary.

The Jim Reaper, as he’s been dubbed by some United fans, has stretched the credulity of accountants with that stance, just as he did when he said the club would have gone bust by 2025 without his intervention.

There are, as Chelsea have proven despite mind-melting operating losses of £673m in the last three financial years, almost always accounting sleights of hand that clubs can use to bend the rules.

From Ratcliffe’s side of the ledger, however, he seemingly doesn’t have the flexibility to, as Chelsea have, sell several hundred millions of pounds worth of assets to themselves to generate artificial profits for PSR.

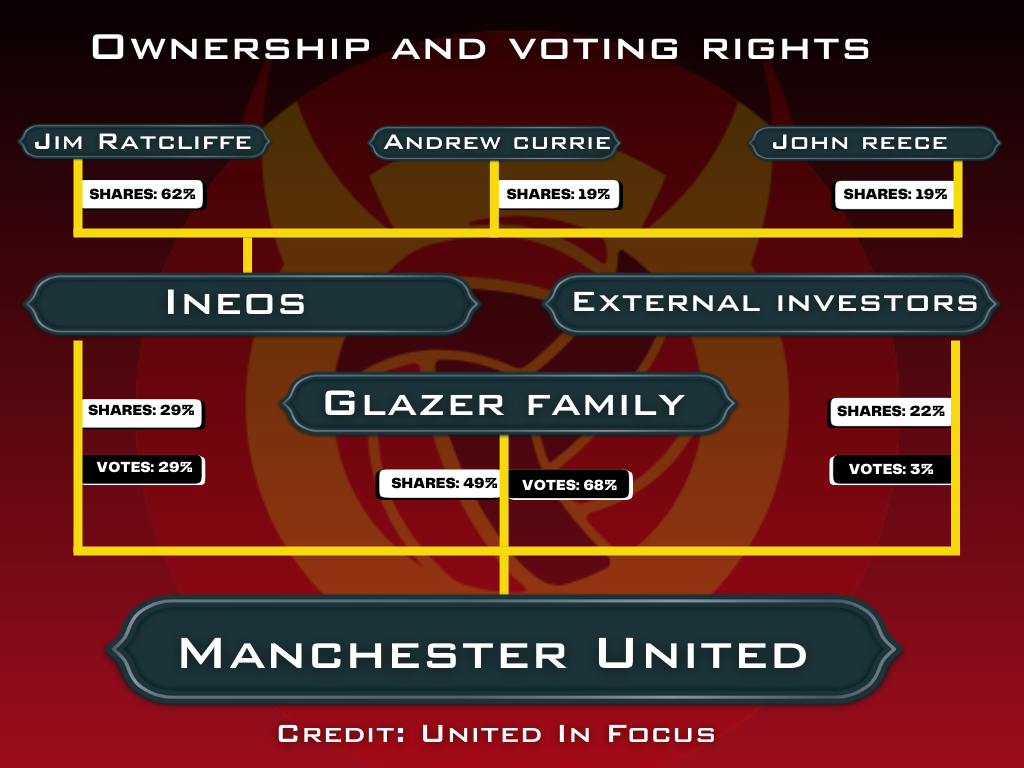

Ineos also have to contend with United being a public listed company, which comes with obligations to external shareholders, who own about 22.5 per cent of the club.

Those shareholders, who include the likes of Lindsell Train and Ariel Investments, are likely thoroughly unimpressed with the club’s debt position, which is a legacy of the Glazers’ leveraged buyout in 2005.

Their total debt currently stands at £731.5m and has left United groaning under the weight of interest payments and, significantly for Ruben Amorim and Jason Wilcox, a huge PSR burden.

But aside from interest payments which could reach up to £50m per year when United are forced to refinance after repayment day in June 2027, another feature of the debt is that it is in dollars, not pounds.

That means that when exchange rates fluctuate for better or for worse, it has an impact on United’s profit-and-loss account, which is how the Premier League assess PSR.

In their most recent set of quarterly results, for example, the club reported foreign exchange losses of £15.9m. In total, around £240m worth of United’s debt is unhedged and liable to this effect.

That was because the dollar weakened against the pound, an effect which many economists think will accelerate with president Donald Trump’s historic programme of tariffs on foreign goods in the US.

Kieran Maguire warns of volatility

The opposite can also happen too. If the dollar strengthens against sterling, United would book a profit. With the margins as tight as they are, that could make or break United’s PSR compliance.

Speaking exclusively to UIF, University of Liverpool football finance lecturer Kieran Maguire explained: “United are more susceptible to exchange rate movements because their debt is in dollars.

“I think this illustrates that there is a positive and a negative to being registered in the Cayman Island and listed in New York.

“These loans aren’t due for repayment in the short term, but when they do refinance then you’d expect interest rates to be around six per cent. It will certainly hit them.

“Foreign exchange gains and losses don’t have an impact on cash flow but they do have an impact on PSR at present.”

Could salvation be on the horizon with new Premier League squad cost rules?

Because PSR is based on profits and losses rather than revenue, United’s debt is a millstone in the transfer market and the wage budget.

However, if the Premier League moves to a revenue-based system similar to UEFA’s, the debt wouldn’t be relevant in terms of the spending rules, although it would still be a very real business issue.

As it happens, clubs recently voted 19-1 against brining in a new revenue-based model which would have limited spending on wages, transfers and agents’ fees at 85 per cent of turnover and player sale profits.

That is likely due to uncertainty around Manchester City’s ongoing legal battles with the Premier League. Many experts believe a revenue-based system could therefore be introduced in time for 2026-27.

That would be just in time for United, as their interest costs will likely soar in 2027, when £548m of their debt is due for repayment and will need to be refinanced.

“This could be another reason that United are in favour of the squad cost control rules,” suggests Maguire.

“That would side-line the PSR issues that have been brought on by the Glazers’ leveraged buyout and the £1bn in interest and dividends that have seeped out of the club in the last 20 years.

“It looks bad on paper and there is volatility. On the other hand, if the markets turn against the United States, this could be beneficial.

“I do expect the loans to be rolled over at a higher rate and that is going to be a bigger issue than exchange gains and losses.”

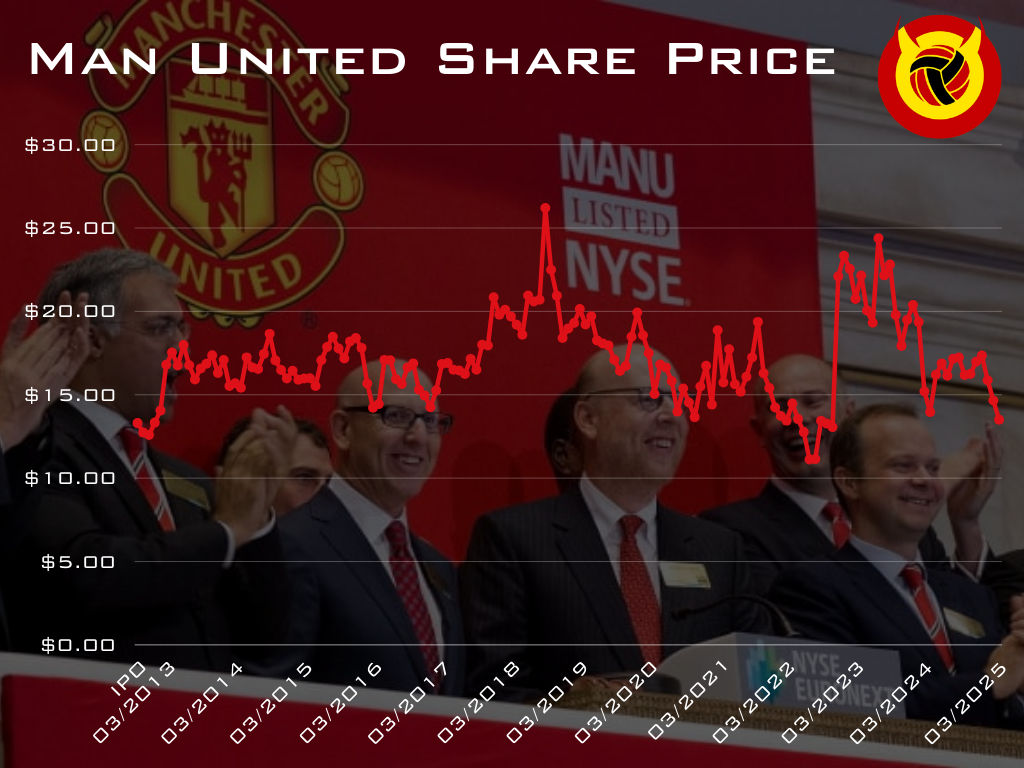

One of United’s biggest investor sells 700,000 shares

Elsewhere, Lindsell Train, the investment firm who were once United’s second biggest investor after the Glazers, have been cutting back their stake in the club.

Last Friday, they confirmed via official New York Stock Exchange documentation that they have sold a further 700,000 shares, which is about 13 per cent of its stake in the business.

That followed a series of similar dumps in 2024, with the group having slashed its ownership in half since 2021.

This reflects decreasing confidence in United as an investment, and perhaps in football club valuations more broadly.

In fact, the share price is lower now than it was in 2012, when United first floated on the Stock Exchange.

With no dividends for institutional investors for several years now, mounting losses, and a woeful season on the pitch, the value of the club as an investment isn’t immediately apparent.

In 2012, Morgan Stanley pulled out of the underwriting process for United’s initial public offering, citing reservations over the Glazers’ £1.5bn valuation of the stock. Perhaps they were right.

Receive a digest of our best United content each week direct to your mailbox