Ineos are part of the problem, not the solution – that was a core message in Manchester United fans’ protest against the club’s owners on Sunday, one delivered with typical Mancunian irreverence.

Sir Jim Ratcliffe was in the house as United drew 1-1 with Arsenal at Old Trafford later that day. A decent point in isolation, albeit one that brings forward Liverpool’s coronation as Premier League champions.

When the Red Devils won their record-extending 20th league title in 2012-13, it was almost inconceivable that their arch rivals – who finished 7th that term – would soon be considered the best run club in Europe.

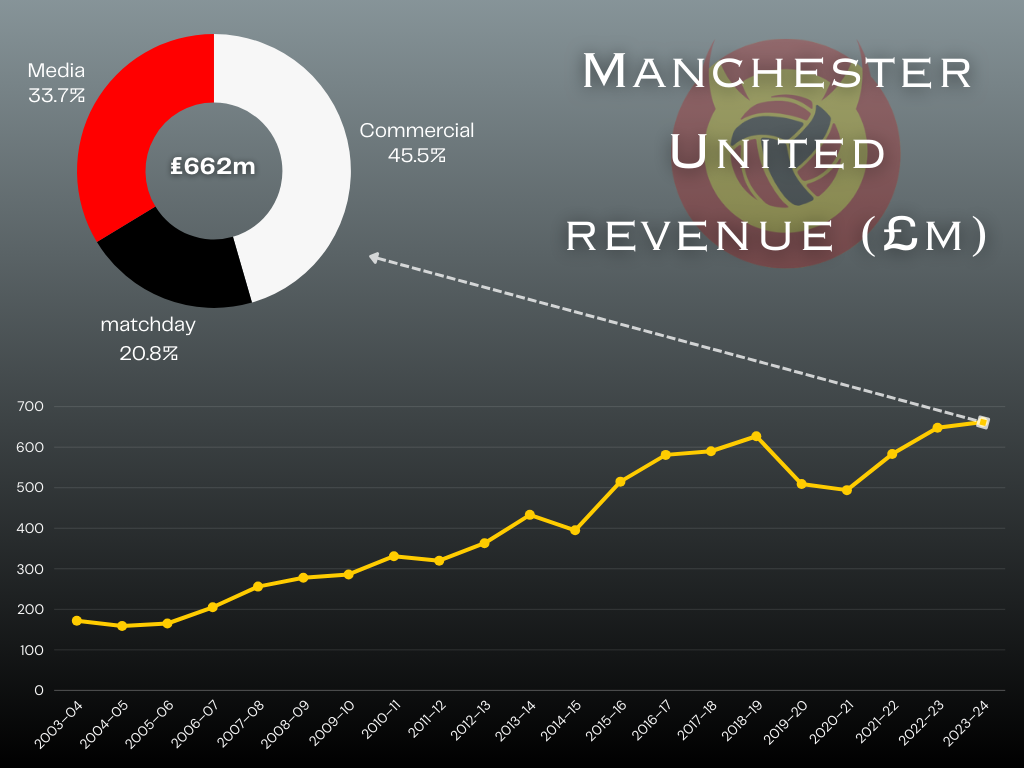

Fenway Sports Group, who bought Liverpool in 2010, paid around £300m in the takeover from Tom Hicks and George Gillett. At the same time, most experts placed United’s enterprise value at around £1.5bn.

15 years later, Premier League club values have exploded thanks to a TV deal that is the envy of every other league on the planet and a commercial revolution in how clubs metabolise fan interest into cash.

United under the Glazer family, however, have been the ugly duckling of the so-called ‘Big Six’ in terms of the rate of their growth.

They are now valued at around £4.8bn, which equates to a compound annual growth rate of about 8 per cent since 2010. In the same period, Liverpool’s annual growth has been over 19 per cent.

Chelsea, Tottenham and Manchester City’s appreciation in value meanwhile has been even more dramatic.

Admittedly, United have come from a higher base and, as the saying goes in finance, elephants don’t gallop. But at around eight per cent, you would have been better off putting your money in the S&P 500.

And if the trajectory continues, United’s position as England’s most valuable club will be under threat very, very soon. In terms of revenue, Liverpool, Arsenal and Man City will earn more than them in 2024-25.

So far, this information could have been lifted directly from an Ineos presentation outlining why drastic cost-cutting measures at Old Trafford are, in their view, entirely necessary.

Behind every redundancy, player sale, and repriced ticket is a different tale of Glazer negligence, mismanagement, or rampant profiteering.

But the placards and chants from Sunday’s protest against the owners prove that fans won’t stand for the hollowing out of their club by Ineos, who many see as the Glazers 2.0.

The goodwill from last February’s £1.2bn part-takeover has been burned through – with interest.

And with Ratcliffe’s chemicals company reportedly struggling with liquidity and debts of their own, do they have the facilities to turn things around in M16?

UIF spoke exclusively to football finance expert, author and podcast host Kieran Maguire for his analysis.

- READ MORE: Bruno Fernandes was excellent but 37-touch Man United star dominated Arsenal at Old Trafford

Core financials strong, says expert, but Man United need more cash injections

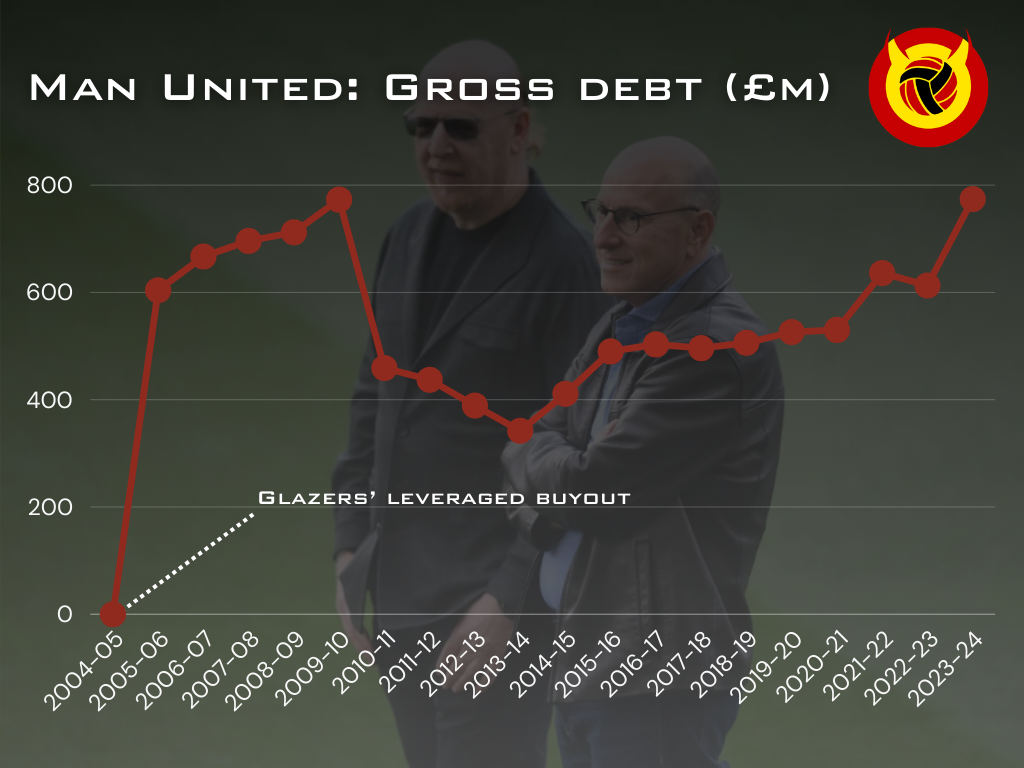

Much like Man United themselves, who have £548m worth of loans to repay before June 2025, Ineos are believed to have a high debt-to-equity ratio that is making access to finance more difficult.

They have taken on debt to cover Project One, a new chemicals plant in Belgium which is set to open in mid-2026. Until then, cash is expected to be tight.

With a new stadium still to fund at Man United, the credit agency Fitch recently revised their rating to ‘negative’.

“I don’t think they will be looking for a 100 per cent mortgage for the new stadium and there will have to be some form of internal funding,” says Maguire.

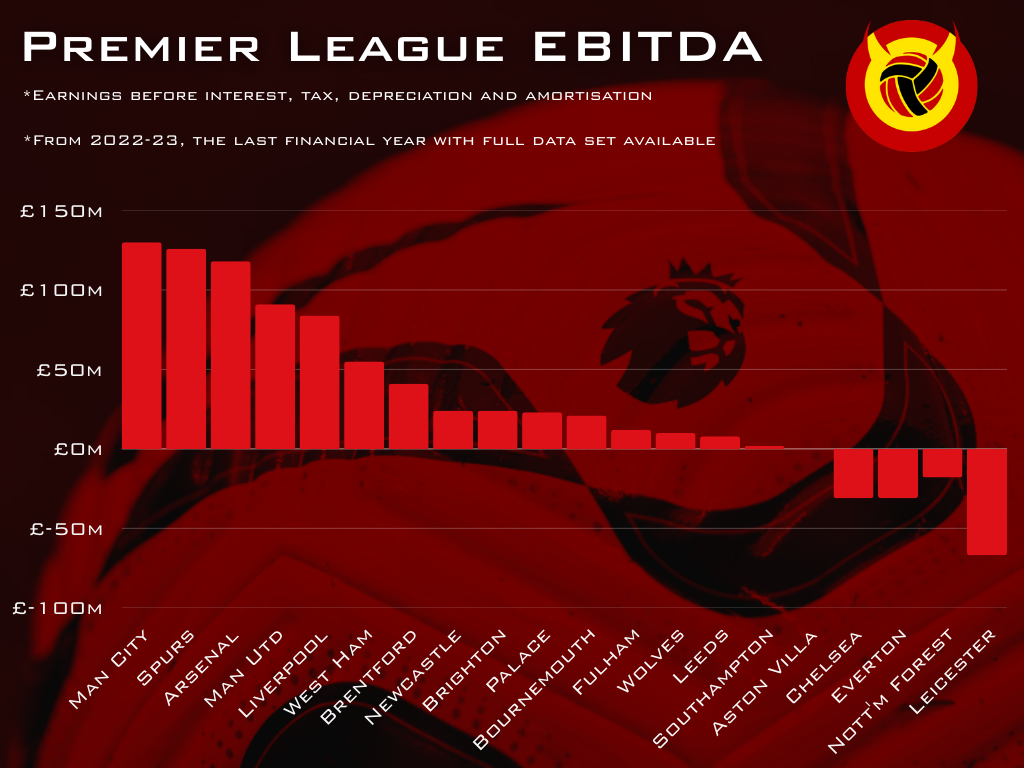

“At the same time, it should be noted that in United’s Q2 report, they were looking to be at the top end of their projections in terms of EBITDA, which is about £140-160m.

“That’s effectively cash that can be used for these purposes.”

EBITDA stands for earnings before, interest, tax, depreciation and amortisation.

It is usually considered a more reliable test for underlying business performance than ‘profit’, the metric according to which United are in the red by almost £350m since 2019-20.

However, as Maguire later explains, United’s debt means that there is still a huge hole to plug before the club’s relatively strong EBITDA means it can sustain itself, as opposed to subsisting on owner handouts.

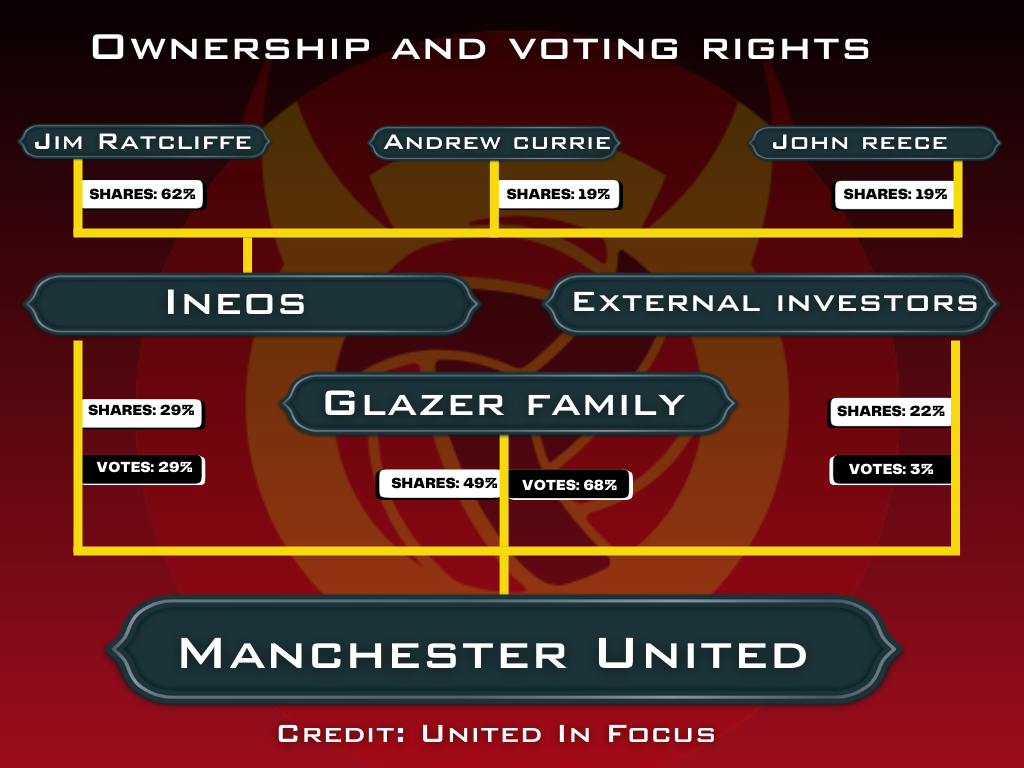

Sir Jim Ratcliffe has insurance option with Ineos equity

Unlike many ownership regimes in the Premier League, Ratcliffe – who turns 73 in October – does not appear to want to make a return on his investment at Old Trafford. At least, not any time soon.

It has been reliably reported that the billionaire would like to increase his stake in the club and, in around six months time, will have the opportunity to match any third-party offer made to the Glazers.

If he is piling his chips high on United as his passion project, could he potentially trade in some of his equity in Ineos to free up cash to cut the club’s debt and scale the budget available to Ruben Amorim?

“United have got themselves into mess,” says Maguire, co-host of the Price of Football podcast.

“They owe huge sums to other clubs for players who have underperformed since Ineos acquired the club. That is a priority in terms of short-term cash flow.

| Date | Position | Player | Team | Reported fee |

| 14 July 2024 | Forward | Joshua Zirkzee | Bologna | £36.5 million |

| 18 July 2024 | Defender | Leny Yoro | Lille | £52.2 million |

| 13 August 2024 | Defender | Matthijs de Ligt | Bayern Munich | £38.5 million |

| 13 August 2024 | Defender | Noussair Mazraoui | Bayern Munich | £12.8 million |

| 30 August 2024 | Midfielder | Sékou Koné | Guidars FC | £1 million plus add-ons |

| 30 August 2024 | Midfielder | Manuel Ugarte | Paris Saint-Germain | £42.1 million |

| 1 February 2025 | Defender | Ayden Heaven | Arsenal | £1 million |

| 2 February 2025 | Defender | Patrick Dorgu | Lecce | £29 million |

“These things will be challenging and it could be that Ratcliffe will have to cash in some his chips at Ineos. I don’t know how much much of his corporate investment and ownership is in Ineos itself.

“But if he sells off 10 per cent of Ineos, he would have the funds. I just wonder whether he would like the thought of doing that because he is a lot smarter than he makes himself out to be in football.”

“It won’t be a disaster because United are a global brand and they have certainty in terms of cash flows from Snapdragon, Adidas and their other corporate partners.

“The new stadium will sell out, they will still sell huge amounts of merchandise, and they will still have a suite of commercial partners that will be the envy of domestic and world football.

“Those cash guarantees will allow them to borrow. I am just concerned that, if I was a lender, would I want to lend 100 per cent of the costs? No, I wouldn’t.”

Recruitment and debt leaves Ineos with £158m financial hole

Analysing United’s cash inflow and outflow situation, Maguire explained: “There are two figures that I tend to focus on: EBITDA and cash from operations.

“EBITDA is the cash from operations on day-to-day business.

“If I was looking at a normal business, I would pay an awful lot of attention to that. What you do with that cash is discretionary – you don’t have to build new factories, pay dividends and so on.

“The problem we have in football is that there are so many legacy purchases.

“Of their £160m EBITDA, if you drop down into their investing cash flow, we see that they are spending more than £140-£160m on transfer instalments throughout the year.

“That then means that, on a net basis, they are needing to acquire funding. That wouldn’t be the case in a traditional business.

“It’s profit if you exclude two huge issues for Man United. First of all, the interest cost and burden of the debt the Glazers have loaded onto the club via the leveraged buyout.

“Secondly, the club’s performance good or bad in terms of player recruitment. Amortisation is your cash cost per season in transfer smoothed out over the contract – and Man United have recruited poorly.

“There have been virtually no successes over the last decade besides Bruno Fernandes.”

Without the Ratcliffe’s equity infusion in the 2023-24 financial year, United’s accounts show that their cash obligations exceeded their earnings by £158m.

That means that Ineos will need to intervene to make sure that it is able to meet its debt obligations, transfer instalments, and other expenses for the foreseeable future.

That can either be in the form of loans to the club, which under new Premier League rules will carry an interest charge in terms of Profit and Sustainability Rules (PSR), or further equity injections.

European Super League: Have Glazers really given up all hope?

When the Glazers were forced to pull Man United out of the European Super League project in 2021 despite years of planning on their end, the family’s business plan for the club had to change overnight.

Had it not been blocked by fans, the breakaway league would have delivered NFL-style profits year-on-year and eliminated the volatility that makes football an unattractive investment proposition for many.

The Super League is back, this time in the guise of the ‘Unify League’. Publicly, United have rejected the efforts by Real Madrid-financed A22 Sports Management to resurrect the competition.

However, A22 CEO Bernd Reichard has this week said that he has spoken to 10 English clubs about playing in the new competition – significantly, he says all were publicly opposed but privately interested.

In truth, the imminent introduction of a government-backed independent regulator for English football will make any attempts by English clubs to join up futile.

Instead, it seems more likely that any clubs A22 have spoken to see the Unify League as a negotiating tactic to secure concessions from UEFA in terms of financial distribution and other governance matters.

Receive a digest of our best United content each week direct to your mailbox